EU, UK sustainable fund disclosure latest

It's time to catch up with the fast-evolving ESG-related disclosure rules facing EU and UK fund firms.

A) EU sustainable finance disclosure latest

1. SFDR update: Level 1 regime

The European Commission (EC) have made several recent statements, regarding the various unresolved SFDR changes facing the EU funds industry.

Addressing a recent EU Parliament (EP) Economic and Monetary Affairs Committee, the acting head of the EC’s Asset Management unit said her EC colleagues will “take stock in the coming months of the outcome”, following the SFDR ‘Level 1’ targeted consultation. Once their “comprehensive assessment” of the current regime is complete, they will provide their successors “with ideas on whether and how the SFDR could be revised”.

Presumably, this means any legal changes to the current SFDR ‘Level 1’ basic law are a matter for the next Commission to decide, after the EU elections (6-9 June 2024).

NB: the EC have now shared the responses received to their SFDR consultation.

Feedback documents and a summary of respondent opinions are now available to download in their website.

2. SFDR update: Level 2 disclosure rules

Separately, Mme. Bussières admitted the EC were unlikely to keep their mid-March deadline to adopt the latest draft SFDR ‘Level 2’ technical specifications, supplied by the EU Supervisory Authorities (ESAs) late last year.

She cited the “the length and complexity of the text” and “internal transition backlogs that need to be covered within the existing EC mandate”; while the EC are doing their “very best to adopt” the draft Level 2 measures “as soon as possible“, there was no mention of a revised approval target date, or a legal application transition period.

NB: a replay of the recent EP ECON meeting can be watched online.

3. Recent SFDR industry position

Following the EC’s recent statement, the European Fund and Asset Management Association (EFAMA) co-signed a letter asking for a “better coordinated approach by regulators” ahead of further SFDR disclosure changes.

Alongside fellow industry organisations, EFAMA requested a ‘holistic’ SFDR legal update process ongoing, i.e.

- Set aside the ESA’s latest draft SFDR ‘Level 2’ RTS;

- Issue one single ‘merged’ RTS, after the ‘Level 1’ legal review is completed;

- Provide firms with at least one year for their transition activities, once the single RTS is legally published.

NB: despite this industry plea, there is no sign the EC intend to halt their interim evaluation of the ESA’s draft RTS, with even more SFDR technical standard changes on the way (after the Level 1 regime review is complete).

Watch this space.

4. Latest SFDR regulatory opinion

“In order to clarify the European regulatory landscape, it would be relevant to focus SFDR on information published at product level and to remove from this regulation any requirement for publication of information at entity level, provided this is adequately covered by the CSRD.”

‘Vers une révision de SFDR’ [AMF position paper, 20 February 2024]

Over in Paris, the French regulator l’Autorité des marchés financiers (AMF) have publicly called for the abolition of the daunting SFDR Entity-level principal adverse impact (PAI) statement. They now support the update of SFDR to a product-only regime, based on “an objective, clear and simple European product categorisation mechanism”.

The EC had asked in their 2023 consultation if the annual PAI statement was “useful”, and whether the “right place” for Entity-level disclosure was the separate Corporate Sustainability Reporting Directive (CSRD) regime.

A recent EU market study claimed that less than 22% of firms have issued an SFDR PAI statement (i.e. obligatory since 30 June 2023). Moreover, many of those published were found to be either incomplete, lacking in detail, or “in some cases left entirely blank”.

B) UK sustainability disclosure and fund labelling latest

1. SDR updates

The Financial Conduct Authority (FCA) recently published a guidance page highlighting the various Sustainability Disclosure Requirements (SDR) and investment labels activities, now underway in the UK.

The SDR policy statement unveiled last November by the Financial Conduct Authority (FCA) was hailed by many as embodying a flexible, “descriptive, not prescriptive” ESG-disclosure regime (compared with the EU-SFDR).

The FCA now suggest local firms familiarise themselves with Annex 2 [‘Overview of SDR and labelling regime’, p.98-121]; however, essential information is located elsewhere, notably:

- Chapter 10: ‘Scope of the regime’ [p.63-68], including ‘Summary of firms and products in scope of the regime’ [table 15];

- Chapter 11: ‘Implementation and operationalising the regime’ [p.69-73], including ‘Summary of implementation timeline’ [table 17]; FCA responses [table 18] and summary section [p.73];

- Annex 1: ‘Principles supporting the regime’ [i.e. “final rules and guidance”, p.91-97], including key concepts [‘Navigating a complex landscape’, ‘Intentionality’, ‘Clear and objective criteria’]; ‘A stylised map’ of the sustainable product landscape [figure 2, p.97];

- Appendix: Made rules / FCA legal instrument [i.e. specific UK regime details, p.137-211].

A reminder that in order to qualify for one of the FCA’s new ‘Sustainability’ labels, prospective funds must:

- invest at least 70% of assets according to their sustainability objective;

- make reference to “a robust, evidence-based standard” (i.e. independently assessed) that is an absolute measure of environmental and/or social sustainability;

- disclose and justify assets held in the fund for other reasons (e.g. cash, derivatives).

Consumer-facing and pre-contractual disclosures must be issued when the label is first used, with specific naming and marketing rules in place. Firms must also follow the standard FCA fund authorisation / amendment due processes.

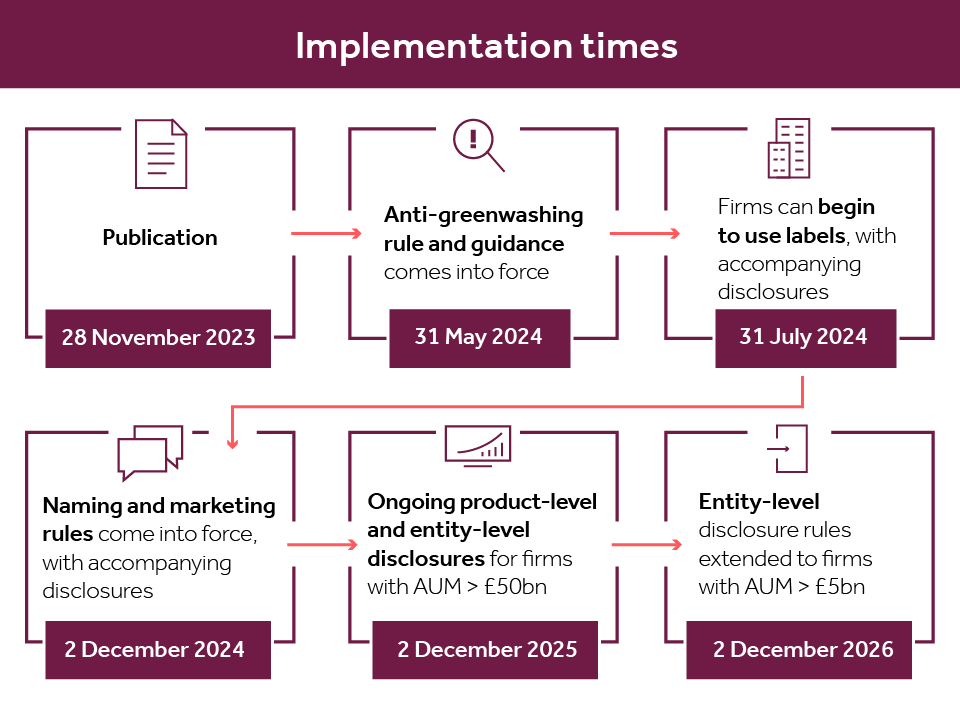

In short, those planning to be part of the SDR labelled-product “first-wave” have scant time remaining to make all the necessary arrangements, to fully align with the FCA’s policy statement, before 31 July 2024.

{kind=link}

2. UK Greenwashing rule update

The first part of the UK-SDR legal package is the local anti-greenwashing rule, set to apply from 31 May 2024.

The FCA’s consultation on their anti-greenwashing rule guidance has ended, with a final version as yet unpublished.

The Investment Association (IA) and UK Sustainable Investment and Finance Association (UKSIF) have raised concerns that firms may not have sufficient time to comply with the FCA guidance. They also highlight further risks arising from the scheduled 6-month gap until separate SDR naming and marketing rules begin to apply for non-labelled products.

Both trade groups now “strongly support” deferring the FCA anti-greenwashing rule application until 2 December 2024.

At the time of writing, the FCA are yet to respond.

3. Overseas Funds Regime: SDR discussion pending

In their SDR policy statement, the FCA state they “want all firms marketing their products in the UK to be subject to the same broad requirements…including those marketing under the Overseas Funds Regime [OFR]”.

However, only the UK Government can legally decide if SDR will be extended to cover non-UK funds.

The UK Treasury (HMT) recently confirmed their intention to consult on whether they should extend SDR scope to include EEA products, within the new OFR. This is expected to occur during Spring 2024. The UK Treasury say they will ensure “adequate time for industry to adapt to any future requirements”.

NB: The HMT statement confirmed they will consider EEA funds within the new OFR to be legally ‘equivalent’ to those based in the UK. An FCA policy lead had previously stated the plan to issue the first set of OFR ‘landing slots’ during April 2024.

4. Other UK association updates

The Investment Association welcome the HMT decision to grant ‘equivalence’ to EEA-UCITS marketed via the new Overseas Fund Regime.

Ongoing, they will continue “to work closely with the FCA on ensuring the application process for investment managers is smooth and efficient and look forward to engaging with Government on the [next] SDR consultation.”

Alongside the regular SDR Implementation Forum for IA members, a new working group has been formed to develop a standard template for the FCA’s new SDR consumer-facing disclosure (i.e. a new, standalone 2 x page document, informally tagged as the “SDR-KID”).

NB: This follows the FCA’s assertion they will only “set out categories of disclosures that firms must make”, while encouraging “development of an industry-led template and industry collaboration on best practice.”

Elsewhere, discussions continue about the need for a simplified local variant of the European ESG template (EET), to reflect the main elements of SDR disclosures covering both labelled and un-labelled products.

More to follow.

5. More UK-SDR to follow, soon

Another reminder that the FCA’s SDR policy statement applies to UK asset managers only (i.e. “a starting point”).

In due course, the FCA intend to “expand and evolve” this new regime to other UK market segments:

- Portfolio management: within the next few weeks, the FCA are expected to consult on revised SDR portfolio management rules. Their original proposals were deemed unsuitable, given “most portfolios are diversified and unlikely to invest only in UK funds with labels”.

- Financial advisers: the FCA will also soon consult on how SDR is applied to the financial advice sector. They recently set up a new independent advice sector working group, to “build on existing capabilities in sustainable finance, including how the SDR and labels support their role”. The FCA will sit as an active observer, having requested the group to supply a ‘good practice’ report during H2-2024.

- Pension and other investment products: the FCA are currently engaging with The Pensions Regulator (TPR) to consider how the SDR regime can be extended to pension products in the “medium term”.

C) latest ESG market trends, opinion

1. Latest key SFDR market statistics

“Investors pull record money from Article 8 funds, while Article 9 funds suffer first-ever quarterly outflows.”

SFDR Article 8 and Article 9 Funds analysis Q4-2023, Morningstar

Morningstar have published their latest quarterly SFDR fund analysis, covering Q4 2023.

Latest key trends detected include:

- ‘Sustainable’ products: market share increase to 0% [€5.2 trillion AUM];

- Article 9 ‘dark-green’ funds: EUR 4.7 billion net QTR outflow (“…first ever”)

- Article 8 ‘light-green’ funds: EUR 26.7 billion net QTR outflow (“…largest on record”).

- ‘Unsustainable’ products: market share decrease to 0% [€3.6 trillion AUM];

- Article 6 ‘non-sustainable’ funds: EUR 15.7 billion net QTR inflow.

- Re-classifications: 218 x art.6 products upgraded to art.8; 4 x art.9 funds downgrades to art.8.

2023 annual SFDR fund flows were:

- Article 9 funds: total inflow of €4.3 billion;

- Article 8 funds: total outflow of €27 billion;

- Article 6 funds: total inflow of €93 billion.

Elsewhere, in their regular ‘Funds Through the Lens of the EET’ section, Morningstar analyse the latest coverage of the three key fields in the European ESG template:

- Minimum % Sustainable Investments: 81%;

- Minimum % Taxonomy Alignment: 63%;

- PAI Consideration: 99%.

2. Latest SDR market forecasts

“We expect conversations in the next few months and the first wave of implementation later this year, to determine how this market will shape up.”

Hortense Bioy, Global Director of Sustainability Research, Morningstar

In their SDR policy statement, the FCA estimated around 280 funds (currently using “sustainability”-related terms in their names and marketing materials) will use their new SDR investment labels.

Morningstar recent analysis paper [‘SDR Through the Looking Glass’] forecasted the prospects of the new UK market for sustainability-labelled funds:

- 300 existing funds [8% of UK domiciled] may adopt one of the SDR labels this year;

- ‘Sustainability Focus’ [46%] will be the most used label, followed by ‘Sustainability Mixed Goals’[31%], ‘Sustainability Improvers’[12%] and ‘Sustainability Impact’ [11%];

- Equity funds [52%] will top the “SDR-labelled product universe”, well ahead of Fixed-income funds [8%];

- The vast majority of UK labelled funds will be actively managed [93%];

- Investor demand and competitive pressure are key stimuli for firms to use SDR labels;

- Funds “with similar aims” are likely to adopt different SDR labels.

It is also assumed that while some UK managers will adopt a “cautious… wait and see” approach, others have pre-judged the SDR regime to be “too constraining”.

3. French retail guidance prompts fund pullout

Late last year, the AMF updated their ‘position-recommendation’ document, which details information expected from local fund firms that “incorporate non-financial approaches” facing retail investors.

Originally published in March 2020, the 23-page document contains specific guidance in many instances, including disclosure of ‘non-financial information’ when presented:

- in the name of the collective investment product; or

- in the KIID or KID; or

- in the marketing materials (e.g. fund factsheets).

The latest AMF rules are deemed by one expert to “go above and beyond the already onerous SFDR standards”, who now advises firms to re-consider the impact of the French rules; these have reportedly forced several fund firms to downgrade / de-register their sustainable products marketed in France.

4. “Divestments” planned ahead of EU ESG-fund name guidance

The European Securities & Markets Authority (ESMA) are likely to finalise their long-disputed ESG fund-naming guidance within the next few weeks. This is likely to apply from Q3-2024 for all new EU fund launches, with a six-month transition period available for pre-existing products to align.

Meanwhile, Bloomberg report that several fund managers are preparing to “adjust their portfolios” within the time available. One large firm is said to be planning to “divest more than 5% of holdings in some ESG funds”, in order to conform with ESMA’s latest ‘Level 3’ guidance.

5. PSF publish ‘compendium of market practices’

Finally, the Platform on Sustainable Finance (PSF), an EC advisory group, have published a ‘compendium’ to demonstrate how the EU sustainable finance framework is assisting the collective transition to net zero by 2050.

This document is a series of market observations from various stakeholders (e.g. corporates, investors, public sector, consultants and auditors), each describing key elements of the EU Taxonomy and SFDR.

A 234-page annex includes investor case studies for each stakeholder group, covering a range of asset classes (e.g. equities, real estate, infrastructure) and market practices (due diligence, transition planning, reporting).

____________________