EU, UK sustainable fund disclosure latest

It's time to catch up with the fast-evolving ESG-related disclosure rules facing EU and UK fund firms.

A) EU sustainable finance disclosure regulation latest

1. EC publish SFDR L1 consultation feedback summary

This week, nearly five months after their “targeted” Sustainable Finance Disclosure Regulation consultation ended, the European Commission (EC) published a report to summarise respondent feedback.

As covered in our earlier synopsis, the EC’s continuing ‘comprehensive assessment’ of the SFDR regime aims to identify “any potential shortcomings”, while “exploring options to improve the framework”; major suggestions included ‘uniform’ Product-level disclosures, simplified principal adverse impact (PAI) rules and a new categorisation system for ‘sustainable’ EU products.

Although responses to their Level 1 Questionnaire were made available back in January, this is the first time the EC has formally commented on collective views expressed, in relation to the main topics presented.

’Key messages’ presented by the EC include:

- “Widespread support” for the broad objectives of the SFDR; but

- “Divided opinions” regarding attainment of regime objectives, so far;

- “Consensus on the need to ensure consistency across the wider Sustainable Finance framework”;

- “Split views regarding the relevance of the SFDR entity level disclosures”;

- “Support for setting uniform disclosure requirements for all financial products”, plus “additional disclosures for products making sustainability claims”;

- “Strong support” for an EU-level voluntary categorisation system, but

- “No clear preference” for either proposed approach, however:

- “Commonly agreed principles for the categories and underlying criteria” have now emerged.

NB: this is an interim EC document, with no proposed SFDR legal amendments, in order to proceed; as mentioned before, next steps are a matter for the next Commission to decide, once appointed after the EU Election process (i.e. with a mandate set to begin from 1 November 2024).

In the meantime, the EC report will be scrutinised by the industry, in the effort to detect any hints of prospective SFDR legal changes in due course.

2. Long-term SFDR regime changes

At this stage, formal publication of draft SFDR ‘Level 1’ regime changes is unlikely before end-2024 / early-2025. Any revised legal text will face prolonged scrutiny by both the new European Parliament and Council of the EU (EP and CoEU), during the standard ‘trilogue’ co-decision procedure.

Moreover, until the final SFDR amendments are published in the EU Official Journal (EUOJ), the European Supervisory Authorities (ESAs) have no mandate to publish any further draft detailed SFDR ‘Level 2’ disclosure specifications; in due course, these will require asset manager consultation ahead of adoption, co-approval and legal application.

As a rough indicator of the SFDR regime due process ahead, last time around:

- Level 1: it took 18 months for the EC’s draft proposed SFDR legal text to be negotiated, finalised and co-adopted, ahead of EUOJ legal publication in Nov 2019;

- Level 2: it then took another 27 months before the ESA’s original draft SFDR disclosure technical standards was industry-assessed, amended, finalised and approved, before EUOJ publication in July 2022.

3. Interim SFDR RTS disclosure rule changes

There is no official news on the EC adoption of the ESA’s draft SFDR ‘Level 2’ technical specifications, supplied last December, following a review of product disclosure and PAI rules back in 2022.

To recap, the 221-page Final Report contains extensively re-designed Product-level disclosure templates, with:

- Key information summary ‘dashboards’ for Pre-contractual and Periodic disclosures;

- New detailed content section for products with greenhouse gas (GHG) emission reduction targets;

- Two new Pre-contractual / Website disclosure templates for multi-option products (MOPs).

The Entity-level PAI statement template was also amended (including ‘Environmental’ and ‘Social’ indicators), alongside disclosure rules for Do No Significant Harm (DNSH) and Derivatives exposures. Moreover, fund firms need to make available all revised disclosure information “in a format which is at the same time human and machine readable” (i.e. XHTML format, using XBRL markup language) in due course.

In the absence of any revised approval target date, it is currently rumoured the EC will adopt most (if not all) of the draft RTS within the next few weeks; however, this must also be formally co-approved by the EP and CoEU.

Moreover, there remains no sign of a formal legal application date (with recent speculation varying between 1 July 2025 and 1 January 2026).

NB: according to our sources, the EC now intends to provide “at least one year” for the industry to prepare their transition to the finalised SFDR RTS disclosure rules, once these are approved and published in the EUOJ.

Watch this space for further developments.

4. CSSF: SFDR remains key local supervisory priority

On 22 March 2024, the CSSF in Luxembourg published a Communiqué to give an overview of their latest ‘supervisory priorities in the area of sustainable finance’.

‘Focus areas’ cover the local asset management industry, investment firms, credit institutions and issuers.

The CSSF will continue to monitor the compliance of Investment Fund Managers (IFMs) with both SFDR and the EU Taxonomy Regulation rules; they will observe ESMA’s supervisory guidance, provided back in May 2022.

Ongoing, specific CSSF asset management priorities relate to:

- Organisational arrangements: including IFM integration of sustainability risks (i.e. following previous UCITS, AIFMD and MiFID II legal amendments);

- Product-level Pre-contractual, Periodic and Website disclosures;

- Fund documentation and Marketing material: where respective sustainability-related information must be consistently disclosed;

- Portfolio analysis: the CSSF will undertake ‘supervisory actions’ to ensure that portfolio holdings reflect the name, the investment objective, the strategy, and the characteristic displayed in the investor documentation.

The CSSF also explain their role in international sustainable finance cooperation, while presenting a simplified overview of sustainable finance supervision exercises (i.e. as planned by the ESAs, based on latest information).

NB: IFMs are reminded that it “remains their responsibility to ensure that the information provided to the CSSF in those different data collection exercises is being kept up to date at any point in time”.

B) Other EU-ESG developments

1. ESMA’s final ESG fund naming rules pending

The recent EUOJ publication of AIFMD II / UCITS VI legally obliges ESMA to “develop guidelines to specify situations where the name of an AIF or UCITS could be unfair, unclear or misleading to the investor. Those guidelines shall take into account relevant sectoral legislation†”.

As indicated in their public statement, this enables ESMA to complete their draft ‘Level 3’ guidelines on ‘fund names using ESG or sustainability-related terms’; these are now expected to be finalised before end-June 2024, reflecting key changes highlighted in December 2023.

ESMA’s sustainable fund naming guidelines will apply to all new product launches within 3 months of formal publication; pre-existing funds will have an additional 6-month transition period to align.

†NB: the revised AIFMD / UCITS legal text also states that “sectoral legislation setting standards for fund names or marketing of funds takes precedence over those guidelines”.

2. EU-CS3D now looms ahead

"Today’s vote is a milestone for responsible business conduct. This law is a hard-fought compromise and the result of many years of tough negotiations. In EP’s next mandate, we will fight not only for its swift implementation, but also for making Europe’s economy even more sustainable.” Lara Wolters, Netherlands MEP (24 April 2024)

The EU Parliament recently approved the draft legal text of a new Corporate Sustainability Due Diligence Directive [‘CSDDD’ or ‘CS3D’]. Several legal firms have described this as a “game changer” for multi-national companies active within the EU.

First proposed by the EC back in February 2022, this regime will apply new rules obliging in-scope companies to mitigate their ‘adverse impacts’ on human rights and the environment (e.g. slavery, child labour, labour exploitation, biodiversity loss, pollution or destruction of natural heritage).

In due course, firms will face a mandatory sustainability due diligence obligation, to be applied across their entire business activity chain. CS3D will also oblige companies to implement a climate change reduction plan that ensures alignment of their business model and strategy with the Paris Agreement; the relevant reporting requirements will align with those of the Corporate Sustainability Reporting Directive [CSRD], in force since 2023.

Companies deemed to infringe their obligations will face civil liability proceedings, alongside minimum penalties of 5% net worldwide turnover.

Once adopted by the Council of the EU, member states have 2 years to transpose the new CS3D text into local law. Firms with over 5,000 employees and EUR 1.5 billion worldwide net turnover will have a 3-year transition period (until mid-2027); the rules will then apply to other companies in a phased manner, depending on their size.

C) UK-Sustainability Disclosure Requirements latest

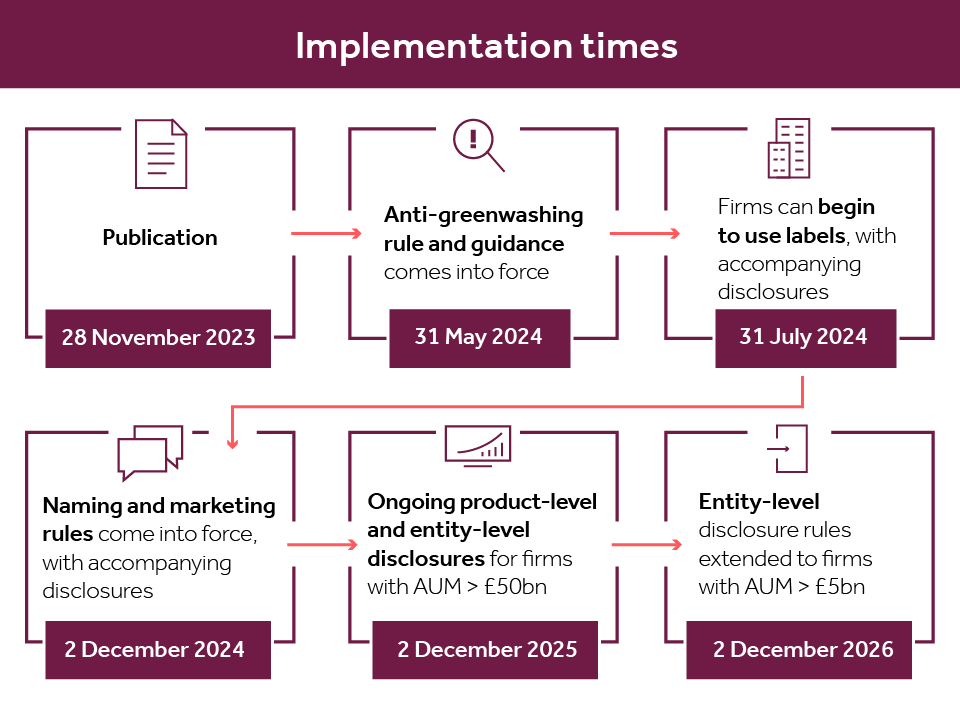

1. FCA publish final Anti-Greenwashing rule guidance

The Financial Conduct Authority recently completed guidance covering the Anti‑Greenwashing Rule [‘AGR’].

The AGR lies at the core of the UK Sustainability Disclosure Requirements (SDR) and investment labels framework, finalised in November 2023.

Despite concerns raised by several UK fund associations, the FCA have now confirmed both their AGR and non-handbook guidance will come into force on 31 May 2024 (i.e. the first major UK-SDR milestone).

{kind=link}

Ongoing, the AGR will apply to all financial products or services communications made available by FCA-authorised firms to UK clients, wherever these refer to environmental and/or social characteristics.

Sustainability-related references “can be present in (but are not limited to) statements, assertions, strategies, targets, policies, information and images relating to a product or service”; these are now expected to be:

- Correct and capable of being substantiated;

- Clear and presented in a way that can be understood;

- Complete – they should not omit or hide important information and should consider the full life cycle of the product or service.

- ‘Fair and meaningful’, in the event of comparisons with other products or services.

All authorised asset managers are in scope, regardless of whether they are subject to the UK Consumer Duty.

NB: The AGR will also apply to UK-approved financial promotions for overseas products and services; one legal firm also advise that EU-UCITS within the temporary marketing permissions regime (TMPR) are in scope, also.

2. SDR, labelling regime: status

Since our last update, the FCA’s SDR and labelling guidance page remains unchanged.

Meanwhile, time is fast-running out for firms seeking to be part of the SDR first wave; those wishing to adopt an SDR label for existing products face an FCA approval period of at least one month to secure approval before 31 July; as before, in order to launch a new “sustainable” UCITS product, there is a two-month application process period.

The Investment Association (IA) recently informed members their template for Consumer-Facing Disclosure (CFD) (developed in collaboration with Eversheds Sutherland) will be formally unveiled within the next week or so.

Separately, we understand local discussions continue about a feasible alternative to the European ESG Template [EET], reflecting the SDR policy statement, to appear within the time available. More to follow.

3. OFR roadmap: placeholders for SDR consultation, legal updates

On 1 May, the FCA and UK Treasury (HMT) co-published their new ‘roadmap’ for implementing the Overseas Funds Regime (OFR), to replace the TMPR as a long-term gateway for EEA-UCITS to be promoted in the UK.

This latest document contains important updates regarding the long-awaited consultation on extending SDR scope to include OFR products; expected to take place during the spring, this is now nudged to Q3-2024.

In addition, there are now key placeholders for potential SDR/OFR legal updates:

- End-2024: GOV.UK to “lay legislation required to implement its decision on SDR & labelling for OFR funds”;

- 2025: FCA “likely to consult on related rules and guidance” (i.e. based on previous item);

- H2-2025: “legislative requirements related to SDR & labelling for OFR funds likely to come into force…the FCA will follow a separate process to make rules”.

4. FCA consult on extending SDR to portfolio managers

The FCA are now consulting on extending the current SDR regime to portfolio management firms.

Their paper includes a summary of proposed rules (p.14-33) alongside draft Handbook text (p.65-100).

The FCA propose to extend all aspects of the UK-SDR framework to those firms either managing investments or providing private equity-related services to clients; the revised scope is primarily aimed at wealth management services for individuals and model portfolios for retail investors, in specific relation to model portfolios, customised portfolios and/or bespoke portfolio management services (i.e. per client preference).

In addition, firms offering portfolio management services to professional clients (or institutional investors) can also choose to opt-in to the new SDR labelling regime.

The deadline for responses is 14 June 2024; the FCA intend to apply SDR labelling, naming and marketing rules (including consumer-facing and pre-contractual disclosures) to these additional firms, from 2 December 2024.

5. EMT revised to flag UK-SDR products

On 22 April, FinDatEx formally revised their European MiFID Template [EMT V4.2] to include supplementary UK-specific information. Alongside optional extra Financial Instrument cost data (added at the suggestion of the IA), there is a new indicator for fund firms intending to produce CFDs, in relation to the UK-SDR regime.

____________________